📑 Quick Navigation

Current trends in sea and air freight – and why your network matters

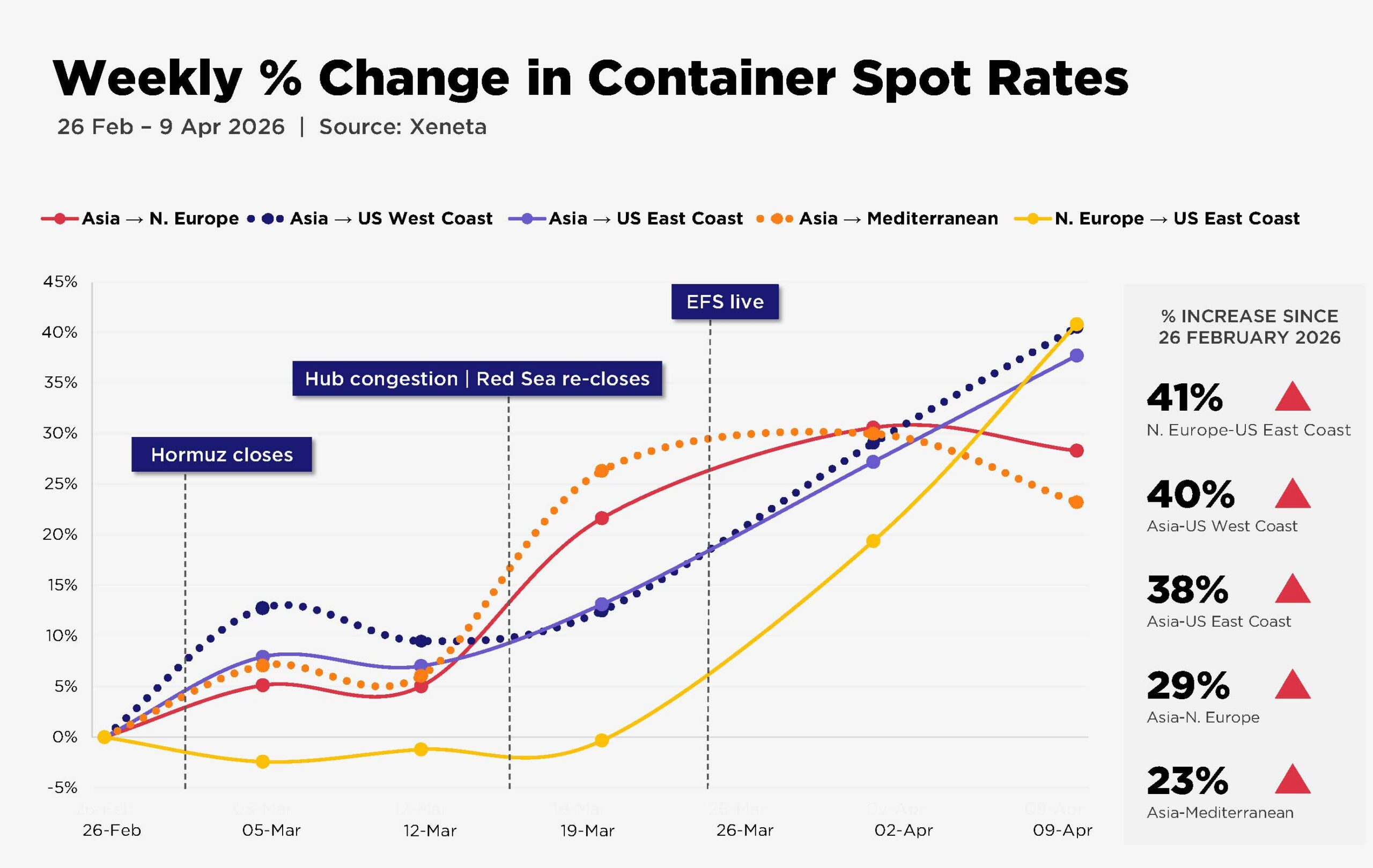

You’d have to go back to 2021/22 to find sea freight rates trending as aggressively upward as they have over the past month. According to Xeneta, container spot rates are up an average of 34.2% since the end of February, and that’s before accounting for the eye-watering increases on Middle East corridors.

As industry veterans know, periods like this are a stress test: for supply chains, for carriers, and for the relationships that underpin the international moving sector.

From the Gulf to the globe: how we got here

Shrinking quote validity windows, surcharge flurries, rates that spike week over week – in many ways the impact of the conflict feels like Covid all over again. But where the pandemic increase was demand-driven, the reasons for the current surge are structural.

Cape rerouting is now priced into 2026 rates by default, a clear sign that shipping lines don’t expect to transit the Suez Canal any time soon. To offset the rising oil price, they also implemented emergency fuel surcharges (EFS) across all lanes at the end of March.

The effect of these was immediate, with even the Northern Europe–US East Coast corridor – normally among the most stable – recording successive weekly increases of approximately 20%.

Air freight rates have likewise risen sharply on the back of increased demand, constrained capacity, and higher fuel costs.

South and Southeast Asia have been worst affected. Emirates, Etihad, and Qatar Airways handle approximately 50% of cargo for these regions, and the reduced capacity has increased spot rates by 50-100% since the end of February. Equally Gulf-carrier reliant, Africa’s capacity to Europe is down 40% and rates up 20% for the same period.

In complex conditions, relationships move cargo

During the pandemic, overflow sea demand was partly absorbed by air cargo, carriers invested in additional vessels, and ultimately the market corrected. In 2026, air capacity is already strained, and the industry has no influence on the oil price.

It’s precisely when conditions are this difficult that being part of a trusted international community stops being an intangible benefit and starts being a measurable one.

It is our trusted and long-standing relationships with you that allow us to identify optimal routing options, flag rate windows, and move quickly when opportunities arise. In turn, we put the global AGS network – and the extensive expertise of our many local teams – at your disposal.

If you’re facing a logistical dilemma without an apparent solution, please reach out to your AGS contact to see what they can do. In these challenging times, solidarity is fundamental to our industry’s success.

The Middle East impact: AGS network COOs report

Shaped by geography, trade routes, and local infrastructure, the effects of the crisis are being experienced differently in every market. Our Network COOs share their real-time views from the ground.

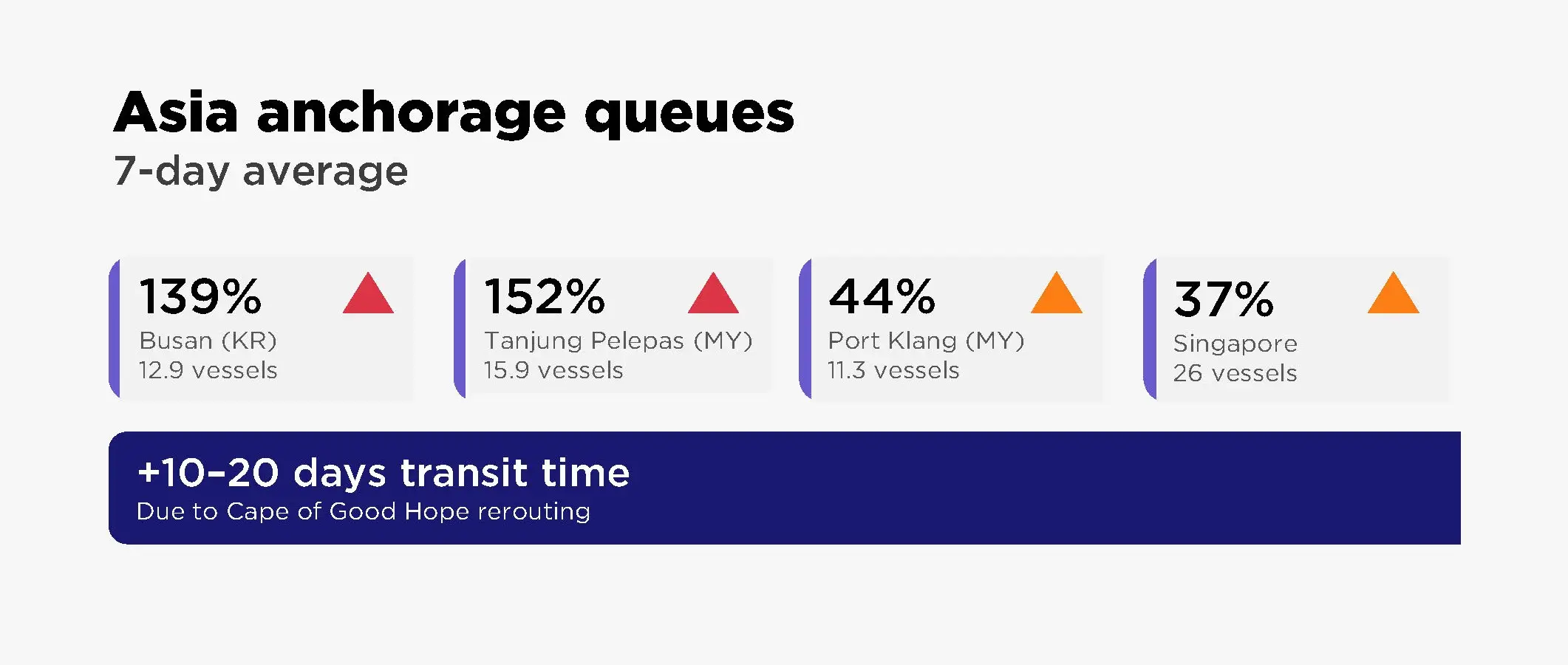

Asia – COO Clement Fagon

Gulf-bound shipments are being discharged in the transshipment hubs of Malaysia and Singapore, but unable to travel onward, are remaining in port. This has resulted in major congestion.

North Asian ports are also congested, although to a lesser degree – mainly due to vessel bunching, as Cape rerouting has disrupted arrival schedules.

India – COO Zia Husain

Vessels diverted away from Middle Eastern ports are being discharged at the ports of Nava Sheva and Mundra, resulting in congestion and consequently delays in berthing and cargo handling.

Extended transit times are creating additional transshipment risks, including cargo rollovers, extra handling, and missed connections. This creates uncertainty in final delivery schedules and overall planning, which is compounded by last-minute operational changes and delays in confirmation from shipping lines.

![]()

Europe – COO Elliot McMahon

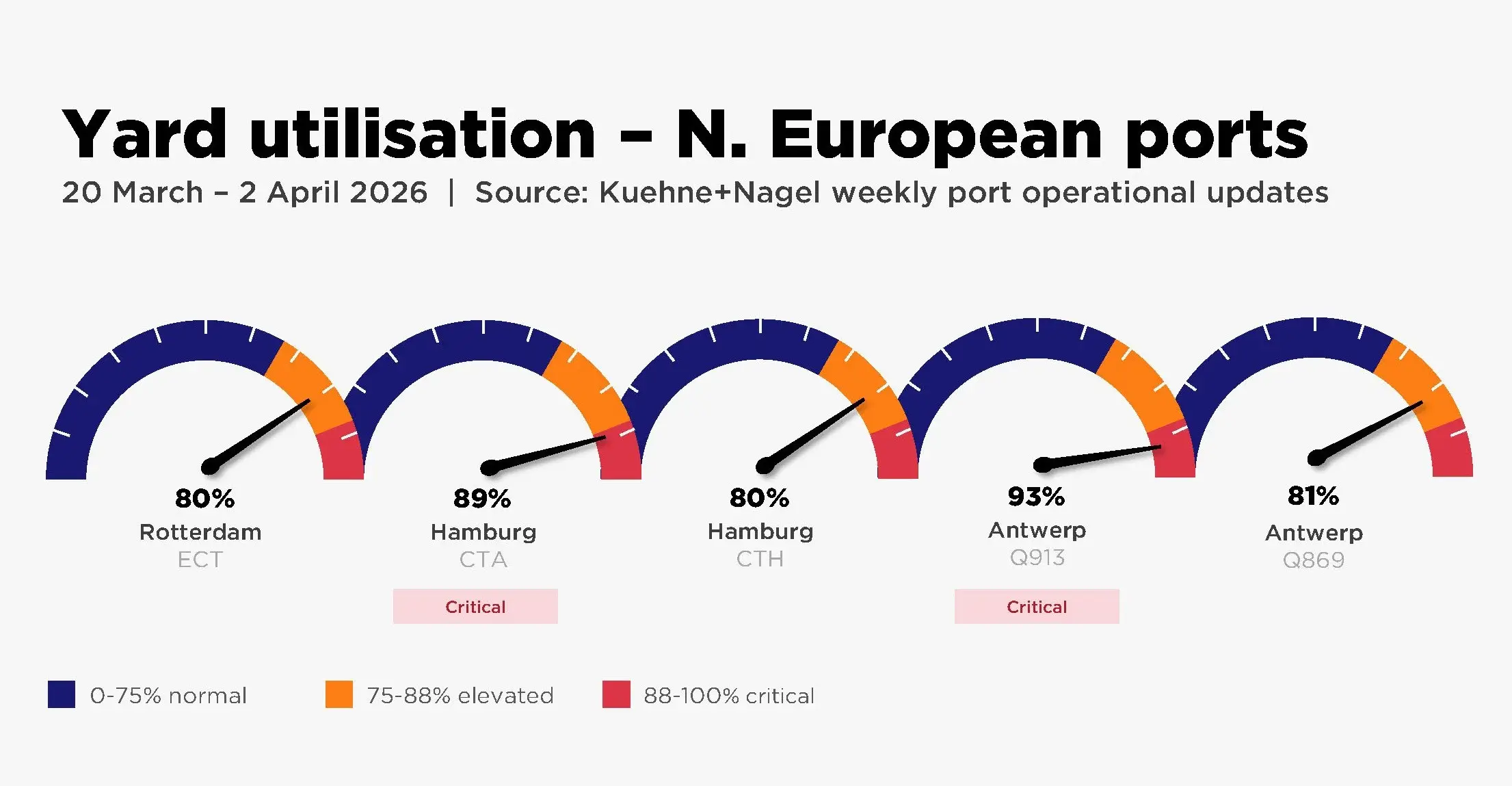

The ports of Rotterdam and Hamburg are experiencing severe congestion as Cape-rerouted vessels arrive in clusters.

Truck capacity to inland distribution points is tightening due to reduced arrival windows. Hamburg is now restricting truck deliveries to 2.5 days before ETA on some vessels.

Antwerp remains a key transshipment hub for feeder services into Eastern and Central Europe and any congestion here feeds into inland timelines.

![]()

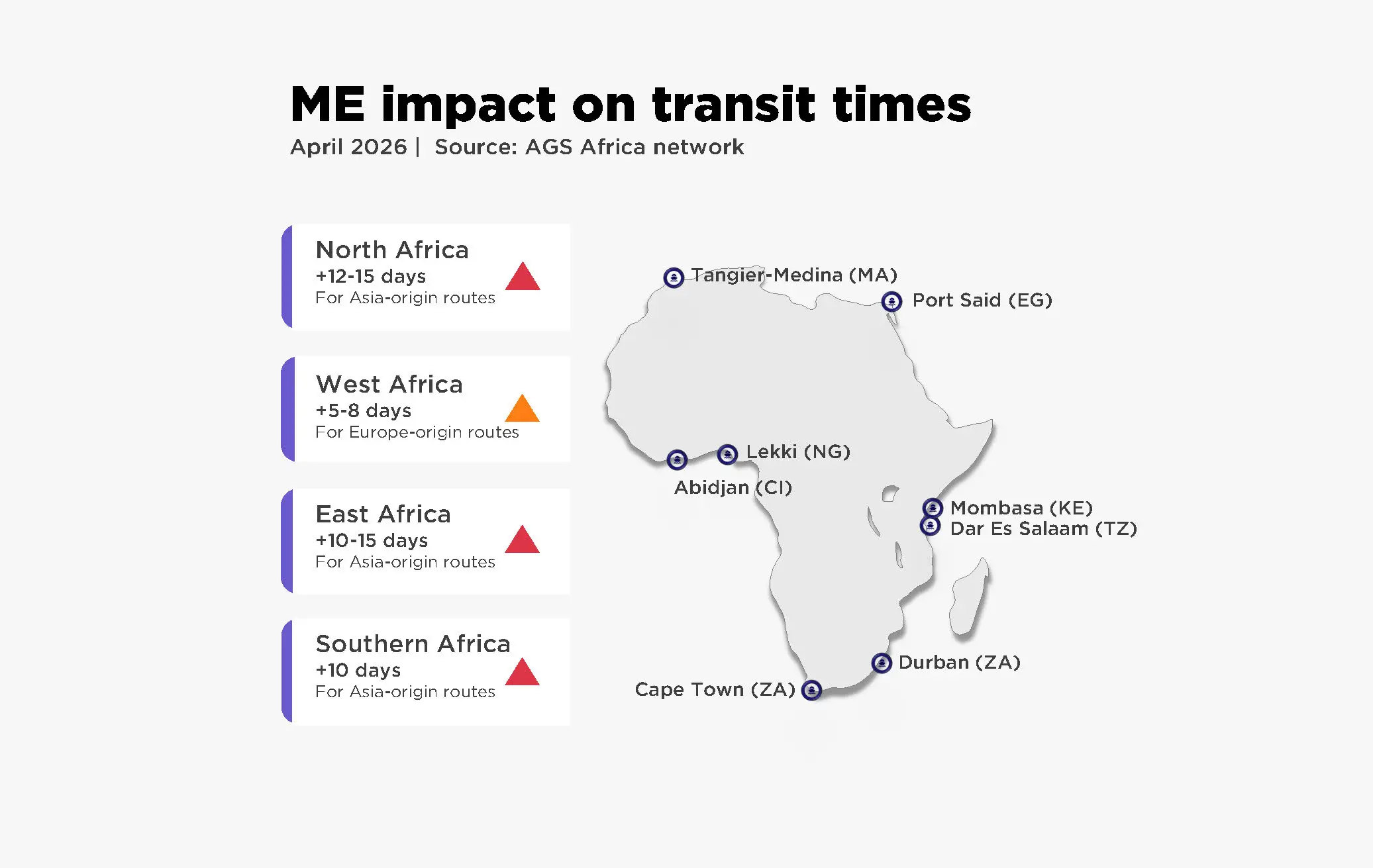

Africa – COO Thomas de Mallmann

Southern Africa

Cape Town has recorded a 112% surge in diverted vessels since early March 2026. Durban is handling 94 vessels/day (+35%), with the Durban–Johannesburg–Zimbabwe corridor at critical congestion levels.

East Africa

Mombasa and Dar es Salaam have emerged as alternative discharge ports following the closure of Jebel Ali. The Mombasa–Nairobi–Kampala–Kigali corridor is under critical pressure, and South Sudan has formally rerouted cargo to Dar es Salaam — though congestion there is comparably severe. Container evacuation to Inland Container Depots now takes 10–14 days, and demurrage charges have risen significantly.

West Africa

Vessel bunching from Cape rerouting is disrupting port approaches. Late-arriving vessels must queue behind on-schedule calls and are discharged subject to berth availability.

North Africa

With the Suez Canal effectively closed, Egyptian port traffic and canal revenues are down approximately 50%. The Moroccan port of Tangier-Medina is actively managing capacity to absorb additional traffic from Cape-routed vessels transiting the Strait of Gibraltar en route to Northern Europe.